Dubai’s real estate market continues to attract global investors due to its strong economy, luxury developments, and high rental returns. Many buyers are interested in Dubai property payment plans because they provide flexible financing solutions that make property ownership more accessible without requiring full upfront payment. These payment structures allow investors, expatriates, and first-time buyers to spread costs over several years while benefiting from Dubai’s growing property market. Developers in Dubai often compete by offering attractive installment options, post-handover plans, and lower down payment requirements to attract international buyers.

Why Flexible Payment Plans Are Popular in Dubai?

Dubai’s real estate market continues to attract investors from around the world thanks to its luxury developments, strong rental returns, and investor-friendly environment. Many buyers are now exploring Dubai property payment plans because they offer flexible financing solutions that make property ownership more accessible without requiring full upfront payment. These plans allow investors, expatriates, and first-time buyers to enter the market more comfortably while benefiting from Dubai’s growing real estate sector.

- Flexible installment options reduce upfront financial pressure

- Easier access to Dubai’s luxury real estate market

- Attractive opportunities for first-time property investors

- Strong long-term investment potential and rental yields

- Supportive regulations for foreign property buyers

- Wide range of residential and commercial property options

- Availability of off-plan projects with extended payment schedules

- Developers compete by offering buyer-friendly financing structures

- Reduced the need to liquidate other investments or savings

- Dubai’s stable economy increases investor confidence

- Payment flexibility allows better financial planning

- Growing demand from international buyers and expatriates

Who Benefits Most from Dubai Property Payment Plans?

- Expatriates: Those who may not have immediate access to large capital but wish to invest in Dubai’s thriving market.

- Young Professionals: Individuals starting their careers who prefer to build wealth through property ownership rather than renting indefinitely.

- Investors: People looking to diversify their portfolios with real estate without liquidating other assets.

- Families: Those planning for long-term stability and wishing to secure a home for their children’s future.

- Business Owners: Entrepreneurs who want to invest in commercial properties but need flexible financing options.

Types of Dubai Property Payment Plans

Dubai’s real estate market offers a variety of payment plans tailored to different buyer needs and financial capacities. Understanding these options is crucial for making an informed decision. Below, we explore the most common types of Dubai property payment plans available in the market today.

1. Post-Handover Payment Plans

Post-handover payment plans are designed for buyers who prefer to take possession of their property immediately but wish to defer payments until after the handover. This option is particularly popular among investors who want to rent out the property while gradually paying off the developer.

How It Works:

- The buyer pays a small initial deposit (typically 1020% of the property price) at the time of signing the sales agreement.

- The remaining balance is paid in installments after the property is handed over, usually over a period of 12 to 60 months.

- Interest rates, if applicable, are often lower compared to traditional mortgages, making this a cost-effective option.

2. Installment Payment Plans

Installment payment plans are one of the most flexible options available in Dubai’s property market. These plans allow buyers to pay for their property in monthly or quarterly installments over an extended period, typically ranging from 12 to 120 months. This structure is ideal for those who prefer a structured repayment schedule without the pressure of a lump-sum payment.

How It Works:

- The buyer pays an initial deposit (usually 1030% of the property price).

- The remaining balance is divided into equal monthly or quarterly installments, which may or may not include interest.

- Some developers offer interest-free plans, while others charge a nominal fee for the convenience.

Types of Installment Plans:

- Fixed Installments: Equal payments over the agreed-upon period.

- Graduated Installments: Payments increase gradually, often tied to the buyer’s expected income growth.

- Balloon Payments: Lower initial installments with a larger final payment at the end of the term.

Advantages:

- Spreads the financial burden over time.

- No need for immediate large cash outlays.

- Can be tailored to fit individual budgets.

Disadvantages:

- Some plans may include interest or service fees.

- Buyers must commit to long-term payments, which may not suit everyone’s financial flexibility.

Best For:

- Buyers who prefer a predictable payment structure.

- Those who want to avoid high upfront costs while still securing property ownership.

3. Mortgage Financing Options

For buyers who prefer traditional financing, mortgage options remain a popular choice in Dubai. While mortgages are typically secured through banks or financial institutions, some developers also offer mortgage-backed payment plans in partnership with lenders. This option is ideal for those who want to leverage their existing assets or savings to secure financing.

How It Works:

- The buyer applies for a mortgage through a bank or financial institution.

- The lender provides up to 8090% of the property value as a loan, with the buyer covering the remaining amount as a down payment.

- Repayment terms usually range from 15 to 30 years, with interest rates varying based on market conditions.

Types of Mortgages Available in Dubai:

- Fixed-rate mortgages: Interest rates remain constant throughout the loan term.

- Variable-rate mortgages: Interest rates fluctuate based on market conditions.

- Islamic Mortgages: Sharia-compliant financing options that avoid interest, often structured as profit-sharing agreements.

Advantages:

- Lower initial outlay compared to a full upfront payment.

- Ability to leverage existing assets for financing.

- Longer repayment periods reduce monthly financial strain.

Disadvantages:

- Requires credit checks and financial documentation.

- Interest rates may be higher than developer-backed plans.

- Early repayment penalties may apply in some cases.

Best For:

- Buyers who prefer traditional banking routes.

- Those who want to maximize their borrowing power.

4. DeveloperBacked Payment Plans

Developer-backed payment plans are structured directly by real estate developers to attract buyers. These plans often come with incentives such as discounts, lower service fees, or extended payment periods. They are particularly popular fooff-planan properties, where buyers purchase a property before it is completed.

How It Works:

- The buyer signs a sales agreement with the developer.

- An initial deposit (typically 1020%) is paid at the time of booking.

- The remaining balance is paid in installments, often tied to the project’s completion milestones.

- Some developers offer interest-free plans, while others charge a nominal fee.

Advantages:

- Often includes discounts or bonuses for early buyers.

- Flexible payment schedules aligned with project timelines.

- No need for third-party financing, simplifying the process.

Disadvantages:

- Buyers must trust the developer’s timeline for completion.

- Some plans may include service charges or administrative fees.

Best For:

- Buyers interested in off-plan properties.

- Those who want to secure a property at a lower initial cost

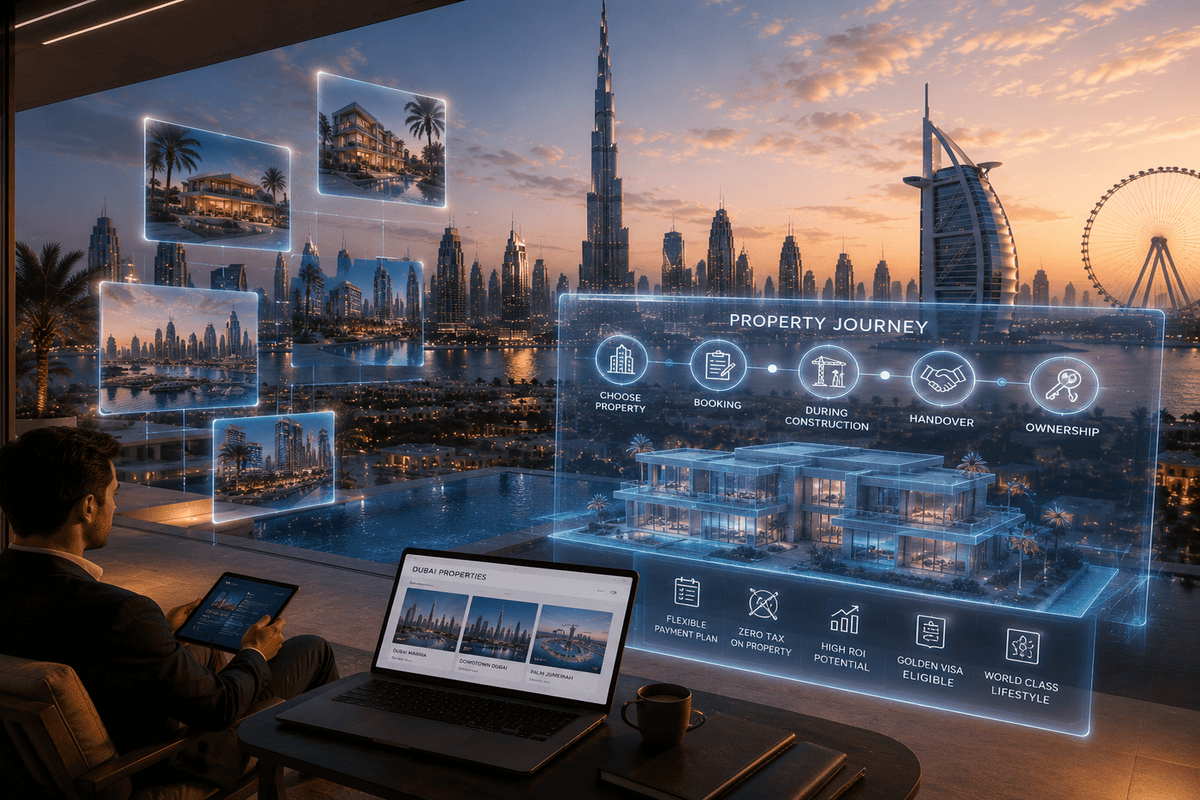

How Dubai Property Payment Plans Work?

Understanding the mechanics of Dubai property payment plans is essential for buyers to navigate the process smoothly. Each plan operates differently, but they all share a common goal: making property ownership more accessible without requiring immediate full payment. Below is a breakdown of how these plans typically function, from initial booking to final handover.

Key Steps in the Payment Plan Process:

1. Property Selection and Booking

- Buyers identify a property and negotiate terms with the developer or seller.

- A sales agreement is drafted, outlining payment terms, timelines, and any associated fees.

- An initial deposit (usually 1030% of the property price) is paid to secure the booking.

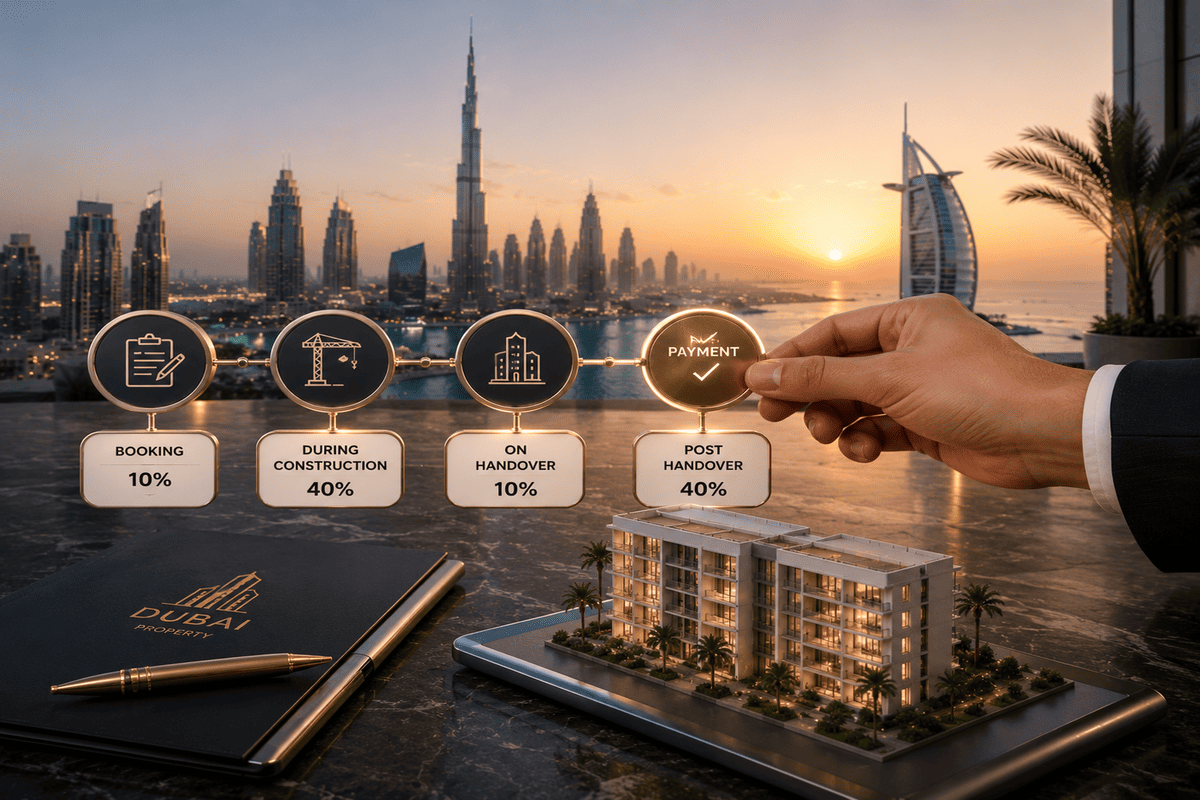

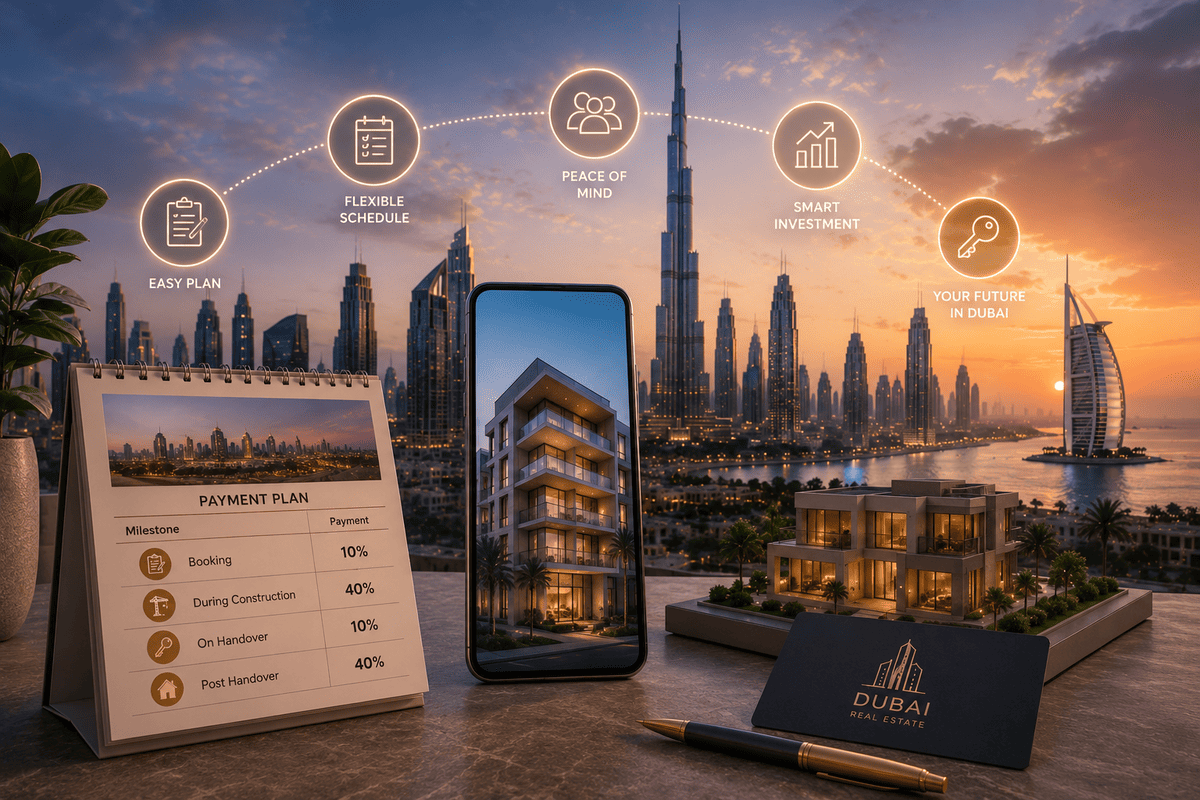

2. Payment Schedule Agreement

The buyer and developer agree on a structured repayment plan, which may include:

- Fixed monthly/quarterly installments.

- Milestone-based payments (e.g., tied to project completion phases).

- Interest-free or low-interest options.

- The agreement specifies penalties for late payments, if applicable.

3. Progress Payments (For Off-Plan Properties)

- For off-plan properties, payments are often staged according to construction progress.

- Developers may release funds in tranches (e.g., 20% at booking, 30% at foundation completion, etc.).

- Buyers receive updates on project milestones to ensure transparency.

4. Final Payment and Handover

- The remaining balance is settled before or at the time of property handover.

- The developer issues the final title deed (for freehold properties) or ownership certificate (for leasehold).

Posthandover, buyers may have additional options like refinancing or mortgage conversion.

FAQs

How long do Dubai property payment plans usually last?

Dubai property payment plans typically range from 3 to 10 years, depending on the developer, project type, and financing structure. Some off-plan developments offer post-handover payment plans that continue even after the buyer receives the property. The duration often depends on the down payment amount and the flexibility offered by the developer or financing institution.

What documents are required to apply for property financing in Dubai?

Buyers usually need documents such as a valid passport, Emirates ID (for residents), proof of income, bank statements, and employment verification when applying for property financing in Dubai. Non-residents may also need additional financial documents and credit history reports. Requirements can vary depending on the bank, lender, or developer offering the financing plan.

How can buyers choose the best Dubai property payment plan?

Buyers should compare payment schedules, interest rates, down payment requirements, and post-handover options before selecting a Dubai property payment plan. It is also important to evaluate the developer’s reputation, project location, and long-term investment potential. Choosing a plan that matches personal financial goals and cash flow can help reduce financial pressure and improve investment stability.